December 8, 2022

The Pros and Cons of an Increased Workplace Pension Contribution

Table of contents

Introduction

Pension contributions and ISAs are two ways to better manage your money in the UK, each with advantages and disadvantages but which is best for you? Below we explore the pros and cons of each, and offer some advice around when might be best to prioritise one over the other, particularly when thinking about retirement (scary, we know).

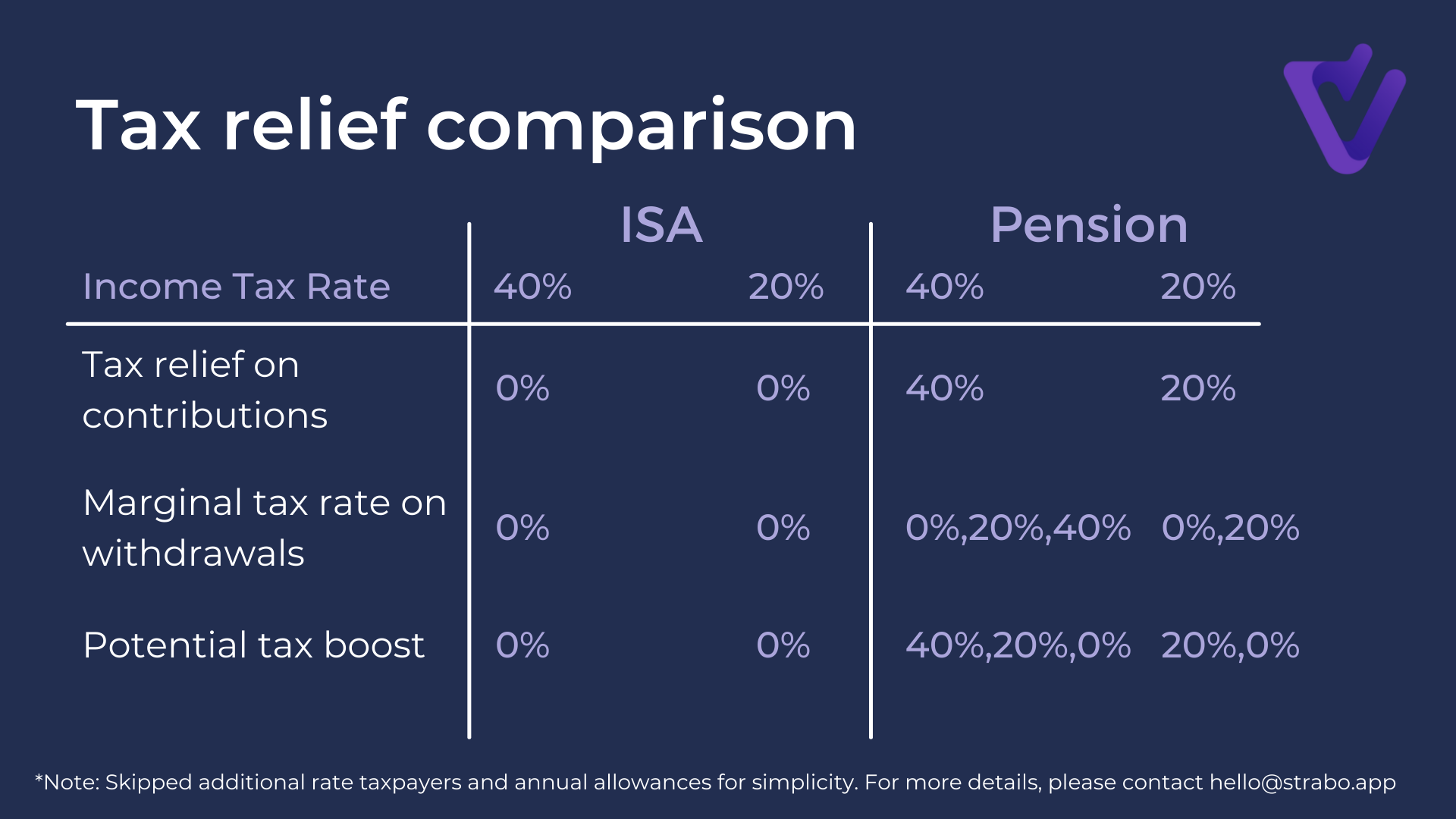

As with much of financial planning, a large factor in these decisions is the tax relief available for each. On a more granular level, this not only differs between pension schemes and alternatives, but also between your personal pension scheme and any occupational pension schemes you may have accrued. These will be supplemented by a state pension and potentially a tax free lump sum that will need to be spread through a number of years.

The Pros and Cons of an Increased Workplace Pension Contribution

When it comes to saving for retirement, increasing your contribution to a workplace pension scheme is a great way to bolster your savings. You will have received documentation on this at point of joining, and are probably contributing to it already. Here are some of the pros of adding to this:

Pros:

- You can save more money for retirement this way, and start definitively contributing to your financial future.

- Your employer may match your contribution, which means you'll get even more savings. This is essentially free money with tax relief!

- The money is deducted from your paycheck before you pay income tax, which can save you money in the long run.

However, there are also some disadvantages of workplace pension scheme contributions:

Cons

- You may not have enough money left over each month to cover all your other expenses. If things are tight, it may be better to build up funds elsewhere first.

- If you leave your job or are laid off, you may have to pay back some of the contribution plus any interest earned. This is unusual but please read the fine print!

- You may not be able to change your contribution amount as easily as you could with an ISA, and this may become a problem if something unexpected occurs or your financial situation changes. It's very much an inflexible solution.

The Pros and Cons of an ISA contribution

ISAs, or individual savings accounts, are a type of savings account that allow you to save money without having to pay tax on the interest you earn. This makes them a great option for savers, as you can make more money this way. We've taken a deeper dive into these in a previous blog post, but include here the salient information. Here are some of the pros of using an ISA:

Pros:

- You can save more money than you could in a regular savings account

- The money is covered by tax relief, which means you won't pay income tax or capital gains tax

- You can access your money whenever you need it. This is the key difference to a pension pot

However, there are also some disadvantages to using an ISA:

Cons:

- The interest rates may be lower than those offered by other types of savings accounts

- You may not be able to add more money once your initial investment is gone

- You may not be able to change the amount of interest you earn as easily as with workplace pension contributions

A comparison

When might be best to prioritise one over the other

It is hard to say when you should prioritise one over the other, as it really depends on your individual circumstances. It may be a good idea to prioritise a workplace pension scheme if you're not able to save a lot of money in a savings account or ISA. You should also prioritise a workplace pension contribution if you are new to saving, or are just starting out on your financial journey.

However, you should consider prioritising an ISA if you have some money saved already and want to maximise the interest your savings earns. It may be a good idea to start out with an ISA of course before graduating to a workplace pension contribution. Whichever option you choose, make sure to contribute as much as you can afford in order to ensure a comfortable retirement. Personally, we like to maximise the matched contributions each month and then feed the rest into an ISA, so that some of this money is available if needed.

Conclusion

The benefit of increasing your workplace pension contribution or even personal pension is the tax relief: you will not be taxed on the money in your total pension pot. The downside to this option is that it can be difficult to decide how much you should contribute and many people do not have enough funds in their budget for retirement savings. With an ISA, if you use a tax-efficient investment like stocks or bonds, these investments will grow faster than with other types of accounts because they come out ahead when invested in mutual funds or ETFs. One downside to choosing this type of account is that there may be restrictions on withdrawals until age 50 but then investors can withdraw up to £10,000/year without paying any penalties (withdrawals over £10k incur a 25% penalty).

This method has proven effective for many people but may not be right for you if you can't commit to putting money away every month.You could contribute the full £2,400/year (the annual max) to your workplace pension account or invest the £1,600/year into ISAs. With an increased workplace contribution, you will enjoy lower taxes and will likely have an easier time sticking to your monthly contributions. However, you will have less freedom over how your money is invested and you may not have enough funds available for retirement savings.

You could choose to invest the full annual £1,600/year in ISAs but this will likely yield lower returns than if you had put it into a workplace pension account. In the end, it is important to weigh the pros and cons of each option and make a decision that best suits your needs!

So to sum up, the decision to prioritise an increased workplace pension contribution or ISA account depends on your situation and the needs of your employer. If you have a difficult time saving money, then increasing your contributions will help ensure that you are able to save for retirement.

However, if you would prefer more flexibility in how funds are invested and don't want them taxed when they come out at age 50+, then contributing all available savings into an ISA may be better suited for you. Ultimately it is up to each individual what option suits their personal financial goals best!

Thanks for reading! We hope this article has been informative and helpful. Please feel free to share any pertinent comments or questions with one of the team. If you have any questions regarding pension savings, or difficult decisions to be made as you approach retirement age, we recommend that you contact your pension provider directly, or engage with a financial adviser.

Check it out today

Get started

Further reading

Company Updates

May 16, 2022

Why We're Crowdfunding

Read more about our decision to launch a Crowdfund with Seedrs

Read article

Investing

May 2, 2023

What is the Best Crypto Portfolio Tracker

Discover how to use Strabo and other tools to track your crypto portfolio across platforms

Read article

Investing

November 19, 2024

Why is there a Crypto Surge and What Does it Mean for my Portfolio

With crypto prices rising across the board, let's take a look at what this means for your portfolio

Read article