May 9, 2022

Best Bank Account for Expats & Digital Nomads: Bank Stack

Table of contents

Introduction

As an expat, banking becomes a challenge. The utility of a bank needs to expand to address our unique goals and it needs to be flexible enough to accommodate our unpredictable lifestyle. We are hesitant to give concrete rankings for the “best bank account for expats & digital nomads" but rather think it's more important to have a banking system in place to accomplish certain goals. We call this a Bank-Stack. A stack of different banks and financial services that work together for you to solve all of your needs. So what are some of those needs?

- Transfer money abroad

- Send money to family/friends in the US (P2P payments)

- Send money to family/friends in the UK/EU (P2P payments)

- Keep/store money in the US

- Receive paycheck/payments and pay bills in the UK

- Manage daily expenses/banking

- Debit card/banking when you travel

The best international current accounts for Expats & Digital Nomads: one or more?

After speaking with over 100 expats across the UK and EU, we found that these are the common needs through which they use banks to solve. We left out investing and credit cards for now for the sole intention of focusing on banking and its ancillary services. In addition, what we found to be interesting is that a majority of millennial expats, and likely a majority of millennials in general, in the UK use one large bank (i.e. Natwest, Barclays, etc) to receive their paychecks into their UK bank account and one challenger bank (i.e. Starling, Monzo) for their day-to-day spend. One rarely forgoes one for the other as there are elements of trust and likeability that come into play. They “trust” the big banks to receive their pay and keep a majority of their savings, but like the functionality and transparency that challenger banks provide. Thus they use both.

Because of these various needs, expats resort to a combination of financial services. i.e. they use X for Y or X for Y and Z. So either they fragment their financial services, consolidate, or a combination of the two. We find ourselves most often in the latter. Some banks/financial services do a great job at doing 2+ things while others are good at a singular job. In addition, it simply boils down to personal preference. Are you a consolidation or a separation fanatic?

Based on your own preference we mapped out different bank-stacks and provided recommended banks/financial services that you can use depending on your preferred stack.

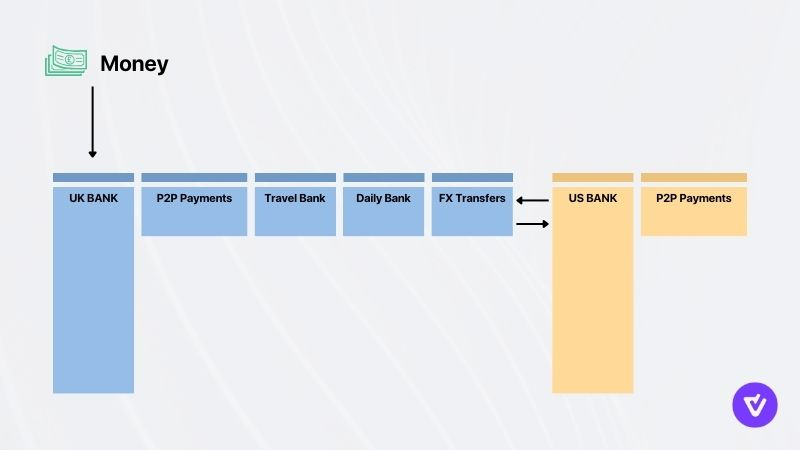

1. The Fragmented Bank Stack

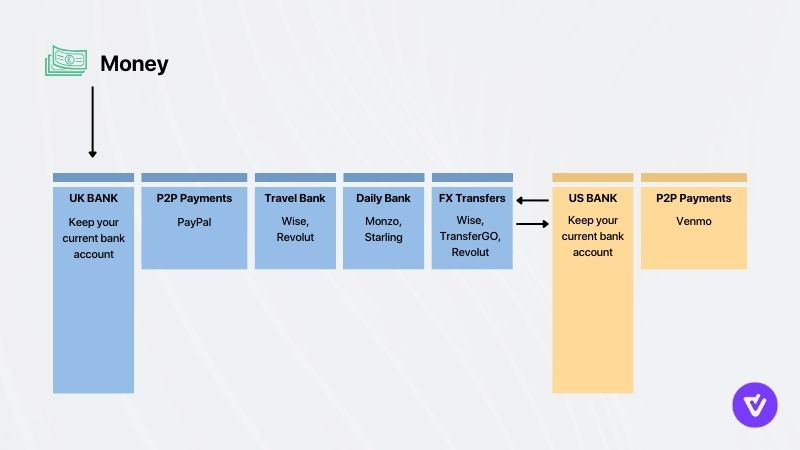

We’ll walk you through the diagram briefly. In this case Jane, a US Expat living in the UK, uses seven banks/financial services to address all of her banking needs. She holds on to her old US bank and uses a separate P2P payment provider to send money to friends and family. She uses her UK bank to receive her pay check/payments, a P2P payment provider to send money to her friends/family in the UK, a travel card to travel and a separate service to send money abroad (fx transfers).

So what’s good and bad about this approach? A 'current account' is used for daily banking needs and a 'savings account' for storing money long-term.

Pros

- One tool for the job

- A philosophical approach to organising and keeping things easily maintainable

- Multiple back-ups (risk mitigation) If one fails or doesn't work in a country while you're traveling, then you have multiple ways to move money around

- You can keep your existing banks rather than closing it out

Cons

- Too many accounts - difficult to track/manage

- Possibility of accruing fees across each transaction vs consolidating some of these functions

So if you:

- Already have existing bank accounts in multiple countries

- Don't want to close out any of these accounts

- Like to have money/risk spread across multiple accounts (risk averse)...

Then this approach is for you and all you'll really need are "bolt-on" services that can execute financial tasks/goals that are unique to your globetrotting life. If this is your preferred method, how could you set up your Bank-Stack with the best bank account for expats & digital nomads? Here's a diagram of our recommendations:

Many share similar features so in the event you lose a card or are locked out of one account while you're traveling the globe, you can be sure to rely on a backup that can sort out your financial needs.

UK & US Banks

Don't need to change: just keep the ones you're using

UK P2P Payments & US P2P Payments

To be honest, there's easier ways to do this but PayPal is a tried & tested platform which makes it easy to move money. So why not use it in the States as well? Simple answer is you can, but again if you want to separate tools for very specific goals, then we'll separate them. Whatever floats your boat. Hence Venmo is a feasible option that is very user friendly and used by millions in the States. The only problem with Venmo is that you won't be able to update the app abroad unless you use a VPN, which is fairly straightforward.

Travel bank

Wise and Revolut still reign supreme in this category. Both offer great fx rates and zero to little foreign transaction fees on purchases or ATM withdrawals. However, we’d rank Wise’s customer service above Revolut’s while I’d rank Revolut’s breadth of travel-related products and user experience above Wise. If you’re looking for a reliable simple card, go with Wise. If you’re looking for more products & services, go with Revolut. Additionally, the benefits of 'foreign exchange' services and the convenience of using a 'foreign exchange app' for efficient currency management while traveling cannot be overstated, offering expats and frequent travelers preferential rates and seamless international payments.

Daily Bank

Monzo and Starling differ in very few ways. You can't go wrong with either in our opinion. There's a few subtle differences but for the most part, they both share features that are important for daily use such as budgeting, getting notifications on transactions, and setting up saving buckets.

Foreign Exchange (FX) Transfers

Wise, Transfergo, and Revolut all provide excellent service to send money abroad. However, if you’re mainly sending from account to account we’d say Wise and Revolut are better options whereas if you’d like to pay for bills abroad then Transfergo has the slight edge. As you can see, there isn’t a one size fits all. The best bank account for expats & digital nomads is actually situation dependent. On the other end of the spectrum you’ll have someone that does not like fragmentation and would prefer to consolidate as much as possible. Here’s what that bank-stack would look like. Utilizing these services for international money transfers and making international payments can significantly reduce the fees usually associated with such transactions, offering the advantage of managing multiple currencies and facilitating seamless global transactions without the high costs.

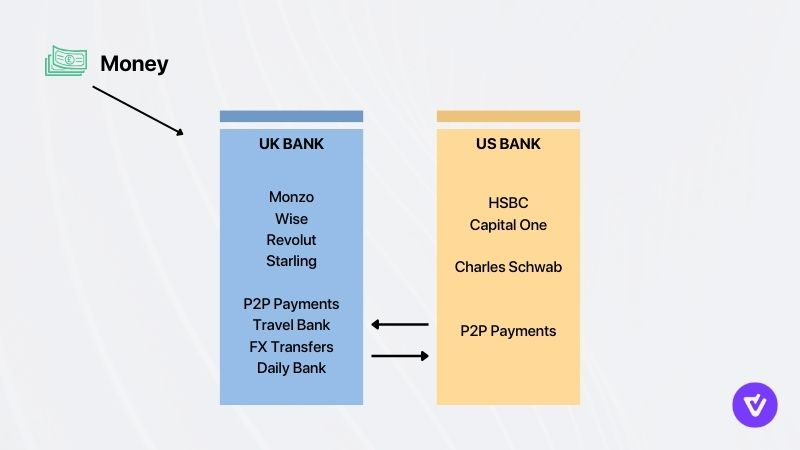

2. The Consolidated Bank Stack

This approach entails that you keep two banks: one in the UK and one in the US. How is this possible? Well challenger banks have improved their product offering over the years, allowing customers to sort out a majority, if not all, of their banking needs in-app. This includes the needs for expats. While there’s still room for improvement, you can definitely make it work if you’re based in the UK.

So pros and cons on this?

A mobile banking app significantly enhances the convenience and accessibility of managing a consolidated bank stack, enabling users to handle their financial transactions and banking needs efficiently while on the go.

Pros

- Two banks for everything = simplicity

- View all bank related expenses in one place

Cons

- Risky: lose or locked out of one, then what?

- Limited on other features that big banks offer (ISA's, Roths, etc)

- Poor foreign money transfers with US banks

This is good for you if you:

- Want to be as minimal as possible

- Don't mind closing your current accounts in the UK

- Simply prefer consolidating features or functions

So here's one way you can set up this Bank-Stack:

UK Bank

Monzo, Revolut, Wise, and Starling do offer enough features and flexibility to sort out most of your needs. The biggest difference would be with Revolut and Wise as you can hold multiple currencies in-app. This makes a strong point for the best bank account for expats & digital nomads of the future: probably the biggest consideration is operating across multiple currencies with low cost. All provide zero to little fees on foreign transactions. In addition, you can receive paychecks into all banks, send money abroad, and pay friends/families easily through email or phone number. For those looking for a more prestigious option, the HSBC Expat Premier Account offers tailored services for international professionals, including a dedicated Relationship Manager and a foreign exchange app. Another notable choice is the Lloyds International Current Account, designed specifically for expats, allowing for easy management of multiple currencies and fee-free international payments. At the time of writing this, Monzo and Starling are licensed banks in the UK whereas Wise and Revolut operate as an e-money institution.

US Bank

HSBC, Capital One and Charles Schwab offer great accounts for expats, allowing you to spend abroad and not suffer high fees or spreads on foreign transactions. However, it is worth noting that moving money abroad is comparatively more expensive than going with a dedicated provider like Wise or TransferGo. HSBC ranges from ~ 5 USD to 20 USD per transaction, Charles Schwab will charge between 15 to 25 USD per transfer and Capital One is up to 40 USD. Whereas Wise and TransferGo can easily save you more than 50% of that. As you can see, there are trade-offs with both approaches above. However, we have found that the middle ground achieves the best benefits of each while keeping things simple and secure. For expats needing tailored international banking solutions, NatWest International offers a robust platform for managing finances across multiple currencies, with 24/7 online and mobile banking, and the ability to make international payments. The NatWest International Premier Account is a premium option for those with specific banking needs, including high earners seeking comprehensive international financial management.

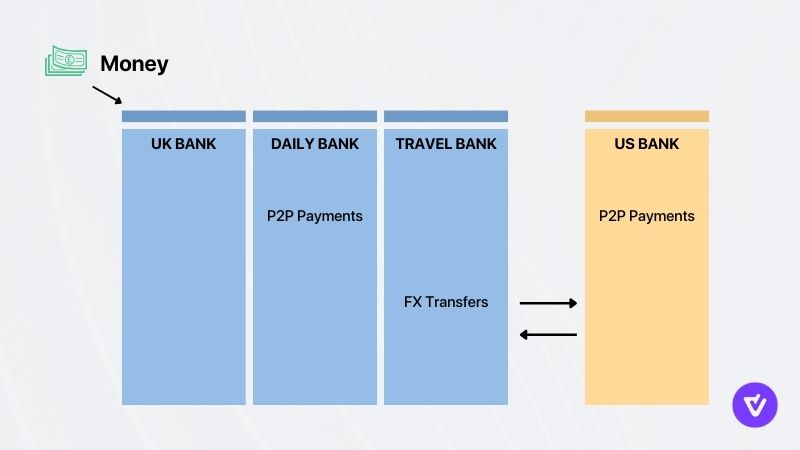

3. Balanced Bank Stack

This setup finds a nice balance between the previous two approaches. It’s diversified enough to spread the risk but simple enough to manage. In addition, it assigns one bank to a specific purpose, making it easier to keep track which account is responsible for each area of your life.

So pros and cons on this?

Additionally, the Standard Bank Optimum Account emerges as a comprehensive banking solution for expats, offering transactional banking in multiple currencies, flexibility across borders, access to foreign exchange, savings, lending services, and digital banking solutions, fitting seamlessly within a balanced bank stack approach.

Pros

- Simple enough to manage

- Each bank has a specific purpose per use case

- De-risk: you have some overlap in functionality so if one bank doesn't work in one country, you have a backup

Cons

- May have to cancel 1-2 banks and open new ones

This is good if you:

- Want a nice balance

- Want to organise per life use case

- Don't mind canceling 1-2 banks

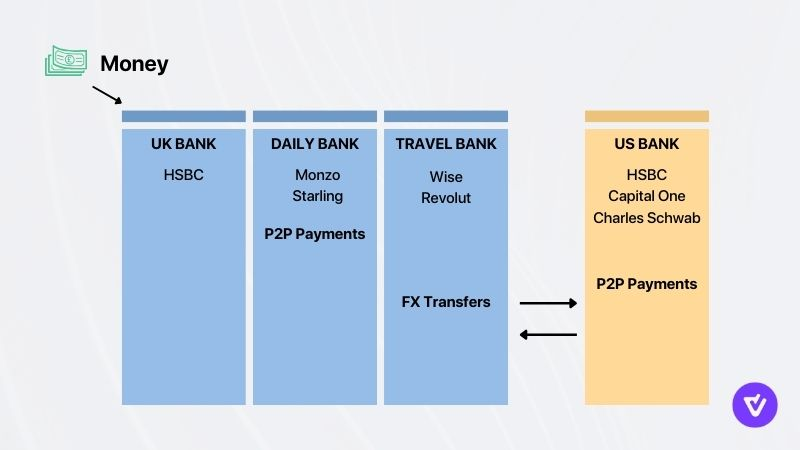

Here's what the ultimate bank stack could be like:

Here's why this is the ultimate setup:

UK Bank

As mentioned above, HSBC is the only institution that has a dedicated expat account for users in the UK. They have little to no fees on foreign transactions, have a global presence and allow its customers to move money between accounts fairly easily. HSBC is generally regarded as the best bank account for expats & digital nomads in the UK.

UK Daily Bank

Monzo and Starling both provide great bank accounts for daily use. They both offer great budgeting features, alerts/notification, P2P payments, and even fx transfers. You can also open multiple saving buckets and purchase additional products in-app

Travel Bank

Wise and Revolut both offer a great travel card that supports multiple currencies along with foreign money transfers. Wise's proposition is much more simple and straightforward whereas Revolut offers more selections of products/services like travel insurance, investing and budgeting features.

US Bank

HSBC, Charles Schwab or Capital One all provide similar offerings however since HSBC is global, I do think it offers more flexibility than Charles Schwab. However Charles Schwab reigns supreme in customer service and reliability, as their card works across several different currencies and charges no fees on foreign transactions. In addition, all integrate with Zelle so you can easily send money to your friends and family back home.

Conclusion

Overall there isn't really a best bank account for expats & digital nomads, but rather it's more important to choose which bank-stack makes the most sense for you and then pick and choose the best banks and financial services that work for you. If there is one requirement that remains consistent across all banks, it is that you'll always want to go with a bank that has little to zero fees on foreign transactions. Whether it be ATM withdrawals or money transfers, you'll want to minimise fees. Banking has gone a long way to reduce fees from seemingly everyday banking activities. There's no reason you should pay exorbitant fees to use your own money. Even if it is thousands of miles away in a different currency.

What's your current bank-stack? What is the best bank account for expats & digital nomads? We'd love to learn more about how you solve the problem so feel free to drop us a line at hello@strabo.app.

Check it out today

Get started

Further reading

Company Updates

May 16, 2022

Why We're Crowdfunding

Read more about our decision to launch a Crowdfund with Seedrs

Read article

Investing

May 2, 2023

What is the Best Crypto Portfolio Tracker

Discover how to use Strabo and other tools to track your crypto portfolio across platforms

Read article

Investing

November 19, 2024

Why is there a Crypto Surge and What Does it Mean for my Portfolio

With crypto prices rising across the board, let's take a look at what this means for your portfolio

Read article